Which ‘local’ company?

So what “local” company is this? It is owned in consortia by:

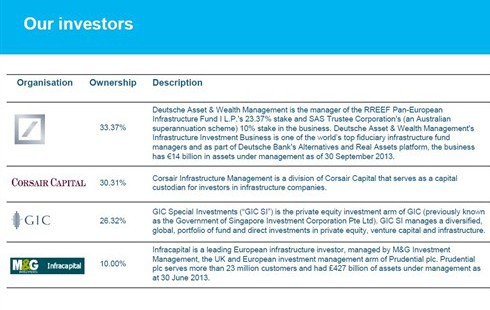

Deutsche asset & wealth management one of the world’s top financial infrastructure fund managers with £14 billion in assets under its management, part of Deutsche Bank’s Alternatives and Real Assets companies, who also own Northern Gas Networks, own 33.37% of the business in association with Super State (the SAS Trustee Corporation – Australia’s largest superannuation scheme) who own 10% of that 33%.

Corsair Infrastructure Management a division of Corsair Capital who have recently acquired Citi Infrastructure Fund (a former owner of our “local” company) for US $3.4 billion, owns 30.31% of the business.

Our local company is partly state-owned – albeit not the British state! GIC Special Investments, the private equity investment arm of GIC, wholly owned by the Government of Singapore, owns 26.32% of the business.

M&G Infracapital, a leading European investor in infrastructure with £2.4 billion investments, and who also own Calvin Capital the exclusive owner and supplier of gas and electricity meters to electricity utilities across England, owns 10% of the business.

The above represents the current owners (according to its website) of our company, and constitute the majority of the original global infrastructure fund consortium partners who acquired the company in 2008.

website) of our company, and constitute the majority of the original global infrastructure fund consortium partners who acquired the company in 2008.

Saltaire Water was the name of that global infrastructure fund; the company they acquired in February 2008 for a reported £5.5 billion was the Kelda Group – the parent company of Yorkshire Water.

The Consumer Council for Water in July 2008 raised no major concerns about the acquisition, but requested an assurance regarding the ownership of Saltaire, remarking that the various holding companies and consortia made it difficult to identify who was actually responsible for the undertaking.

The Kelda Group was de-listed from the London Stock Exchange following its acquisition by the private equity fund consortium Saltaire Water. Public information about the group’s investors is available via the Kelda Group website but is not widely known in the local area.

Yorkshire Water plc was formed as part of water privatisation in 1989. The aim of that privatisation programme was to secure massive new investment in pipes, reservoirs, sewers and waste water treatment works.

Yorkshire Water maintains that it is still a good investment opportunity, with financial investors being attracted by the UK water sector’s regulated base i.e. its monopoly of local customers who have no choice but to use their ‘local’ water company. Investment in Yorkshire Water, the company implies in its Blueprint for Yorkshire strategic objectives document, provides a steady and reliable cashflow with attractive returns for investors.

Residents locally know that investment by Yorkshire Water into its Waste Water Treatment Works has led to rotten and recurring foul odour incidents. The East Riding of Yorkshire Council is currently reviewing those historic foul odour incidents and potential solutions; its special Review Panel is currently meeting behind closed doors and taking evidence from all those involved and having a specific interest in the issue.

Although not the remit of that Review Panel, it is important that the wider issues about the water industry find a forum for debate as well. This article is an attempt to start such a debate.

Is it right that once public-owned companies should now be dominated by aloof international investors who see the supply of local water services as merely an acquisition on a giant Monopoly board game – “I’ll buy the Water Works please!” The counter-argument is that public-owned companies would be at the behest of the rise and fall of particular Government policies of the day i.e. in times of deemed austerity, services would be cut.

Whatever the political arguments, greater public scrutiny of “Yorkshire Water”, its debt and equity investment model, its management structure and an opening of its books to see what investment monies are actually available, must surely be beneficial?

Comments welcomed.

See this on YouTube: https://www.youtube.com/watch?v=peWqu37whs8 and sign the petition at: https://petition.parliament.uk/petitions/762640